Why Compliance in Finance Drives Trust and Stability

- Marensa Advisory

- Jan 24

- 11 min read

Every financial institution in the UAE and GCC region faces the ongoing challenge of keeping up with shifting regulatory expectations while managing serious non-compliance risks. In this environment, a weak compliance function leaves organizations exposed to financial penalties, legal consequences, and loss of trust. By clarifying what compliance really means and how its core pillars work together, you can build a framework that shields your institution and supports sustainable operations, even as local and international standards evolve.

Table of Contents

Key Takeaways

Point | Details |

Compliance as Risk Management | Compliance is a structured function essential for managing non-compliance risk through advisory, risk management, and controls. |

Interconnected Regulatory Framework | Compliance regulations are layered and often overlap; understand this complexity to build an effective compliance function. |

Consequences of Non-Compliance | Non-compliance poses significant financial, legal, and reputational risks, underscoring the importance of a robust compliance function. |

Continuous Monitoring Needed | Regulatory requirements evolve frequently, necessitating ongoing adjustments to compliance policies and processes. |

Defining Compliance in Financial Institutions

Compliance in financial institutions means far more than simply following rules written in a rulebook. At its core, compliance is a structured function designed to manage non-compliance risk through advisory services, risk management, and control mechanisms embedded throughout your organization. In the UAE and GCC region, where regulatory frameworks evolve constantly and oversight intensifies, this definition takes on practical urgency. Your compliance function operates as the guardian against regulatory violations, financial crimes, and operational failures that could damage institutional credibility and attract regulatory sanctions.

The compliance framework within financial institutions rests on three interconnected pillars. First, there’s the advisory component, where compliance teams guide business units on regulatory requirements before decisions are made. Second comes risk management, where your institution identifies threats to regulatory adherence across all operational areas. Third is the control function, which includes policies, procedures, monitoring systems, and audit mechanisms that ensure day-to-day adherence to legal and regulatory standards. These aren’t theoretical concepts. In practice, when a remittance firm in the UAE processes transactions, compliance reviews each pathway against AML regulations. When an investment advisor recommends securities, compliance verifies adherence to investment conduct rules. When a bank opens an account, compliance executes know-your-customer protocols.

What makes compliance distinct from other risk functions is its focus on external obligations. Your compliance team answers to regulators first, then to management. The UAE Central Bank, the Financial Action Task Force (FATF), and various sectoral regulators expect your institution to demonstrate a control environment where risk governance frameworks work alongside ethical compliance standards to prevent misconduct and protect financial stability. This creates a dual responsibility: meeting legal minimums while building an internal culture where regulatory adherence becomes operational habit, not bureaucratic burden. The organizational structure of compliance services varies by institution size and complexity, but the core functions remain constant across financial services regardless of geography. Your compliance function must adapt to your specific business model, customer base, and regulatory exposure, yet the fundamental architecture of advisory, risk management, and control remains constant.

Pro tip: _Map your compliance function’s current structure against the three pillars of advisory, risk management, and control to identify gaps where regulatory risks might slip through unmonitored.

Types of Financial Compliance Regulations

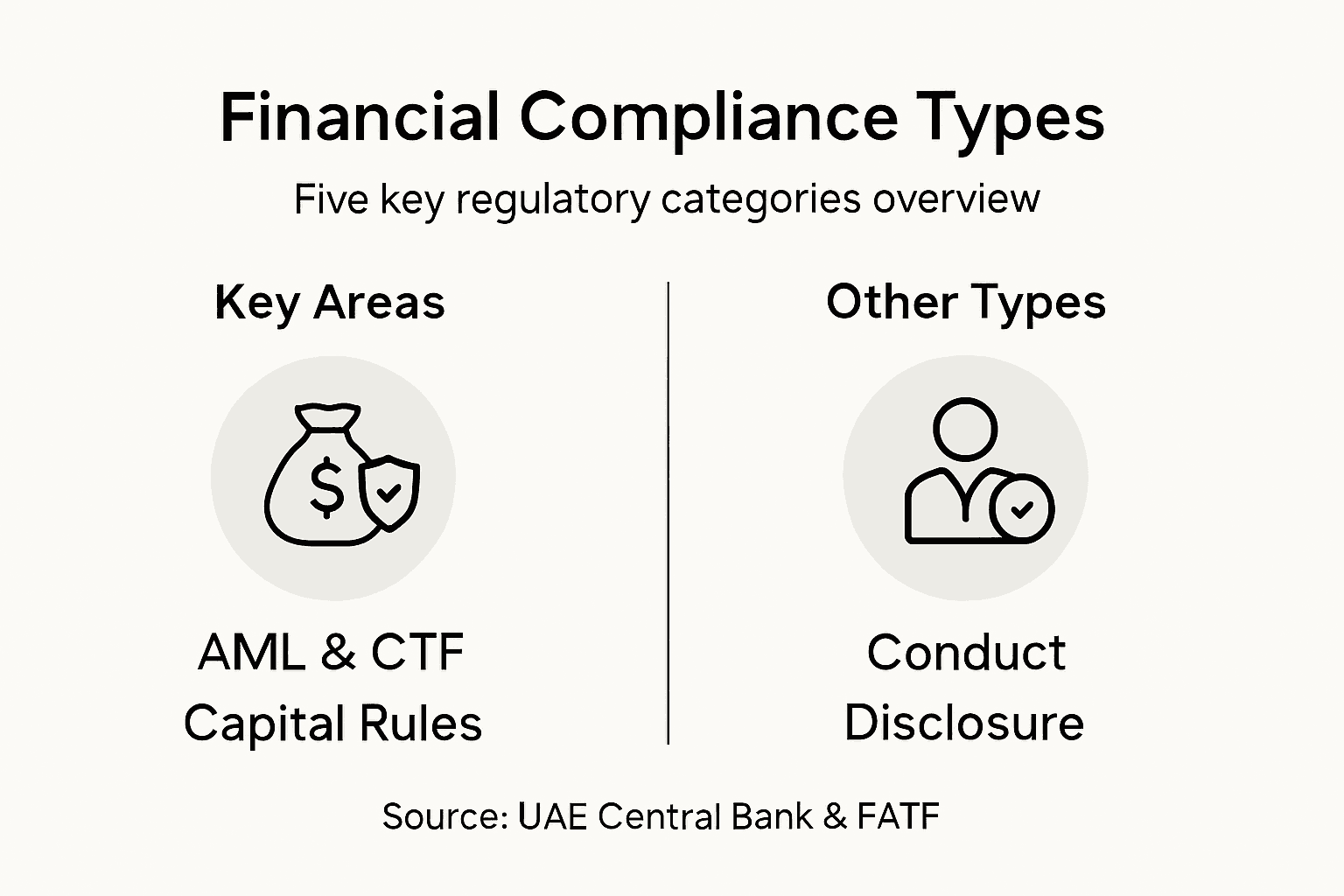

Financial compliance regulations span multiple domains, each addressing specific risks and market failures. In the UAE and GCC region, your institution operates under a layered regulatory framework that combines local requirements with international standards. Understanding the taxonomy of these regulations helps you build a compliance function that addresses each category systematically rather than treating them as one monolithic obligation.

The regulatory landscape breaks down into five primary categories. Anti-money laundering and counter-terrorist financing (AML/CFT) regulations form the foundation, requiring your institution to identify beneficial ownership, monitor transaction patterns, and report suspicious activities. These rules originate from FATF recommendations and appear in UAE Central Bank guidelines that apply across banking, insurance, and investment sectors. Capital adequacy regulations dictate how much capital you must maintain relative to risk-weighted assets, protecting depositors and maintaining systemic stability. Conduct regulations govern how your institution interacts with customers, including rules about transparency, suitability, fair dealing, and complaints handling. Data protection and privacy rules increasingly shape compliance obligations, particularly with regulations requiring secure handling of customer information. Finally, sector-specific regulations vary by your business type; insurance companies follow different prudential rules than banks, while fintech firms face distinct licensing requirements that effective AML compliance tools help address in the UAE context.

What complicates compliance is the overlap between these categories. A single customer onboarding process must simultaneously satisfy AML obligations, conduct rules requiring fair treatment, and data protection standards protecting information. A transaction monitoring system must catch money laundering patterns while respecting privacy boundaries. Your compliance team must map regulatory requirements across these intersecting domains rather than compartmentalizing them. The UAE Central Bank, the Securities and Commodities Authority, and the Financial Action Task Force set overlapping expectations. Global banks operating in the UAE must reconcile local requirements with international standards, sometimes applying the stricter rule when conflicts emerge.

Regulatory requirements evolve constantly. The FATF updates mutual evaluation reports, the UAE implements new anti-corruption standards, and international bodies introduce fresh requirements for digital assets and emerging risks. A static compliance framework becomes obsolete within months. Your institution needs mechanisms to monitor regulatory changes, assess impact on existing controls, and adjust policies before violations occur.

Here’s how key types of financial compliance regulations compare in terms of focus, main requirements, and operational impact:

Regulation Type | Focus Area | Main Requirement | Operational Impact |

AML/CFT | Financial crime prevention | Monitor/report suspicious activity | Implement KYC and transaction checks |

Capital Adequacy | Financial stability | Maintain capital ratios | Manage risk-weighted assets |

Conduct | Market fairness | Ensure transparency and suitability | Enhance client interaction standards |

Data Protection & Privacy | Customer information | Safeguard personal data | Secure systems & data retention |

Sector-Specific | Industry-specific risks | Follow unique industry rules | Adjust policies for each business line |

Pro tip: Create a regulatory obligations matrix mapping each regulation type against your business lines and operational processes, then identify which controls address multiple regulatory requirements simultaneously to maximize efficiency.

Regulatory Bodies and Legal Frameworks

Your compliance obligations do not exist in isolation. They flow from a hierarchy of regulatory bodies and legal frameworks that define what compliance actually means in practice. The UAE and GCC region operates under a multi-layered supervisory structure where central banks, specialized authorities, and international bodies each set requirements that your institution must satisfy simultaneously. Understanding this ecosystem prevents compliance teams from treating regulations as disconnected rules rather than interconnected obligations flowing from specific legal authorities.

At the apex sits the UAE Central Bank, which oversees commercial banks, Islamic banks, and finance houses operating in the Emirates. Below that sit sectoral regulators: the Securities and Commodities Authority for investment activities, the Insurance Authority for insurance operations, and the Financial Services Regulatory Authority for the Dubai International Financial Centre. Each issues directives, regulations, and guidelines that create binding obligations. When the Central Bank updates its AML/CFT guidelines, your institution must revise policies, retrain staff, and adjust monitoring systems. When the SCA issues new requirements for suitability assessments, your investment advisory function must demonstrate compliance through documented evidence. The legal framework establishing these regulatory bodies flows from Federal Law and Emirate-specific decrees that grant them authority and enforcement power. This legal foundation means regulatory requirements carry legal force, not merely advisory status.

Beyond the UAE, your institution faces international expectations. The Financial Action Task Force sets standards that the UAE implements through domestic regulation, creating a two-layer obligation. Mutual Evaluation Reports assess whether the UAE meets FATF standards, and shortcomings trigger international pressure for stronger controls. If you operate across the GCC, you navigate regulatory requirements in Saudi Arabia, Qatar, Bahrain, Oman, and Kuwait, each with distinct regulatory bodies and legal frameworks. What complicates this further is that legal frameworks and regulatory authorities establish rights, responsibilities, and enforcement mechanisms that must be understood not just as compliance checkboxes but as foundational structures defining your institution’s legal obligations and market conduct expectations.

The interplay between these bodies creates both clarity and complexity. Clarity comes from written regulations that specify requirements. Complexity arises when regulatory bodies issue conflicting guidance, when local requirements diverge from international standards, or when enforcement priorities shift. Your compliance function must monitor regulatory bodies actively, interpret guidance correctly, and adjust controls before violations occur. Regulatory scrutiny intensifies when institutions fail to interpret legal frameworks accurately or when they treat compliance as reactive rather than anticipatory.

Pro tip: Establish a regulatory intelligence function that monitors statements, circulars, and guidance from the UAE Central Bank, your sectoral regulator, and FATF so you identify emerging requirements before they become enforcement priorities.

Key Compliance Obligations and Processes

Compliance obligations translate into concrete processes that run continuously through your institution. These are not one-time checkbox exercises. They represent ongoing activities embedded into operational workflows, risk management cycles, and governance structures. Your compliance function performs three interconnected types of work: advisory services that guide business units before decisions are made, risk management activities that identify threats to regulatory adherence, and control processes that ensure day-to-day compliance with legal and regulatory standards.

The core compliance processes your institution must maintain include policy development and maintenance, where compliance teams create written policies translating regulatory requirements into organizational rules. These policies must be current, specific to your business model, and accessible to employees who must follow them. Next comes employee training and awareness, ensuring staff understand their compliance obligations and the consequences of violations. When the UAE Central Bank issues new AML guidelines, your institution must train front-line staff within specified timeframes and document that training occurred. Risk assessment and monitoring form the third pillar, where compliance systematically identifies threats to regulatory adherence across your business lines and implements controls to mitigate those threats. Transaction monitoring systems catch suspicious activity. Customer due diligence procedures verify beneficial ownership. Sanctions screening flags high-risk transactions. These processes run daily, not annually. Finally, reporting and corrective action mechanisms ensure compliance communicates issues to management and the board, and that remediation occurs when violations are detected.

What complicates these obligations is their scale and interconnection. A mid-sized bank in the UAE might operate under 40+ distinct regulatory requirements simultaneously. Each requirement triggers policy obligations, training obligations, and monitoring obligations. Employee turnover means you train replacement staff constantly. New product launches require compliance assessment before launch. Regulatory changes demand policy updates within weeks. Your compliance function operates as an ongoing governance function responsible for advisory, risk management, and supervisory control processes that must adapt continuously. Technology increasingly plays a role here, with automation handling transaction monitoring, sanctions screening, and routine reporting. But judgment remains essential. A compliance officer must decide whether a customer relationship carries unacceptable reputational risk. A compliance team must interpret ambiguous regulatory guidance. These decisions cannot be automated.

The efficiency challenge grows as regulatory expectations expand. Post-2008 financial crisis reforms added layers of compliance obligations. ESG requirements now sit alongside traditional AML and conduct rules. Cybersecurity obligations intersect with data protection rules. Your compliance function cannot simply add staff proportionally. Instead, compliance must leverage technology, process efficiency, and risk-based approaches that focus resources on highest-risk areas. But this efficiency must never compromise effectiveness. A compliance failure exposes your institution to regulatory sanctions, criminal liability, and reputational damage.

Below is a summary of key compliance process pillars and their business purpose:

Process Pillar | Primary Purpose | Example Activities |

Advisory | Guide decisions on regulations | Regulatory guidance, policy input |

Risk Management | Identify/mitigate compliance risk | Risk assessment, monitoring |

Controls | Enforce daily compliance | Auditing, reporting, ongoing review |

Pro tip: Map your institution’s compliance obligations against your business processes to identify where controls overlap, then consolidate them into integrated workflows that satisfy multiple regulatory requirements through single control activities rather than duplicative processes.

Risks, Liabilities, and Impact of Non-Compliance

Non-compliance in finance is not a theoretical risk. It carries concrete financial, legal, and reputational consequences that can destabilize an institution. When a financial institution fails to meet regulatory obligations, it exposes itself to multiple layers of liability simultaneously. Regulators impose fines. Courts impose legal penalties. Stakeholders lose confidence. Customers withdraw funds. Staff leave. The damage accumulates and compounds. Understanding these risks should motivate compliance investment, not as a cost center but as a protection mechanism.

The financial impact of non-compliance operates at scale that commands board attention. Regulatory fines for non-compliance can reach hundreds of millions of dollars, with major institutions worldwide paying billions cumulatively over the past decade. A UAE bank failing to implement adequate AML controls faces potential fines from the Central Bank ranging from millions of dirhams upward, depending on violation severity and duration. But fines represent only the direct penalty. Regulatory investigations consume internal resources. Your compliance team dedicates months to document review, interviews, and evidence collection. Business lines halt operations pending regulatory approval. Technology systems undergo forensic review. Legal fees accumulate. Consulting fees mount. A single investigation can cost an institution millions beyond any fine ultimately imposed. Then comes operational disruption. When regulators identify compliance failures, they often impose restrictions on business activities. A bank might face prohibitions on new customer acquisitions, limitations on product launches, or requirements to divest business lines. These restrictions reduce revenue precisely when the institution is trying to recover from the investigation.

The liability dimension extends beyond financial penalties. Senior management faces personal accountability. In the UAE and across the GCC region, regulatory frameworks increasingly hold executives personally liable for compliance failures within their scope of responsibility. A Chief Compliance Officer could face criminal charges if the institution fails to implement adequate AML controls. A Chief Risk Officer might face sanctions if risk governance proves inadequate. This personal accountability creates incentives for compliance that extend beyond institutional concerns. Board members also face scrutiny. Regulators examine whether boards exercised adequate oversight of compliance, and board members can face restrictions on future directorships or banking sector participation if oversight proved inadequate.

Reputational damage represents the final, often most severe impact. When a compliance failure becomes public, depositors question whether the institution can be trusted with their money. Correspondent banks distance themselves from the institution, reducing access to international payment systems. Investors sell shares. Credit rating agencies downgrade the institution. Employees question commitment to values and compliance culture. Customers migrate to competitors perceived as safer. This reputational damage persists long after fines are paid and investigations close. Trust, once damaged, requires years to rebuild.

Pro tip: Document your compliance program’s effectiveness through audits, testing results, and remediation records so regulators observe genuine commitment to control rather than compliance as reactive response to violations.

Strengthen Your Financial Institution’s Compliance Framework Today

Navigating the complex regulatory landscape of the UAE and GCC region requires more than just understanding rules. It demands a comprehensive compliance function that integrates advisory, risk management, and control to protect your institution from costly penalties and reputational damage. If you want to transform compliance from a reactive burden into a strategic driver of trust and stability, Marensa Advisory is here to help.

Our specialized governance, risk, and compliance advisory services are designed to build robust internal controls and regulatory frameworks tailored to your business needs. Don’t wait until costly fines or regulatory restrictions threaten your operations. Act now to implement practical AML/CFT frameworks, risk-based compliance processes, and effective licensing support. Visit Marensa Advisory and discover how our expertise in regulatory navigation can safeguard your institution’s future.

Frequently Asked Questions

What is the role of compliance in financial institutions?

Compliance in financial institutions manages non-compliance risk through advisory services, risk management, and control mechanisms to ensure adherence to regulations and protect institutional credibility.

How do financial compliance regulations differ across categories?

Financial compliance regulations cover several categories, including anti-money laundering, capital adequacy, conduct, data protection, and sector-specific regulations, each focusing on different operational risks and requirements.

Why is compliance important for trust and stability in finance?

Compliance builds trust by ensuring that institutions follow legal obligations and ethical standards, which prevents misconduct and enhances the stability of the financial system while safeguarding customer interests.

What are the consequences of non-compliance in financial institutions?

Non-compliance can lead to significant penalties, including regulatory fines, legal liabilities, reputational damage, and operational disruptions, which can severely impact the institution’s stability and customer confidence.

Recommended

Comments